Individual Income Tax Return for Income from Production and Business Operations

Individual industrial and commercial households, operators of enterprises and public institutions as contractors or lessees, and sole proprietorships, partners of partnership enterprises shall, in accordance with relevant laws and regulations, file individual income tax (IIT) returns for income from production and business operations.

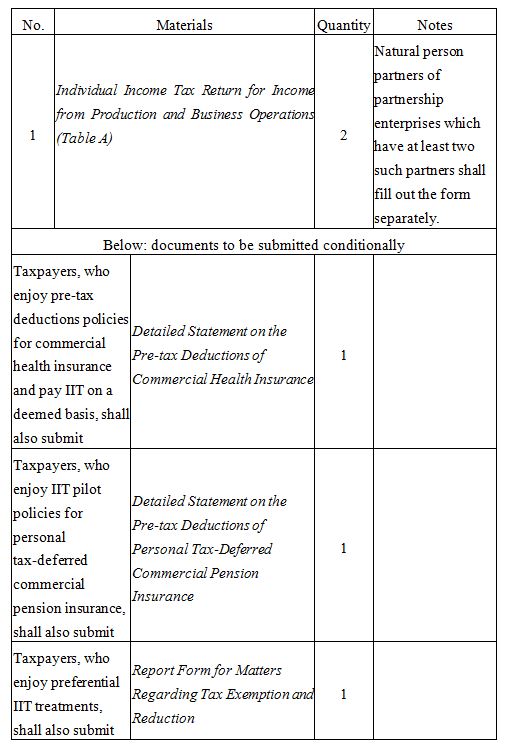

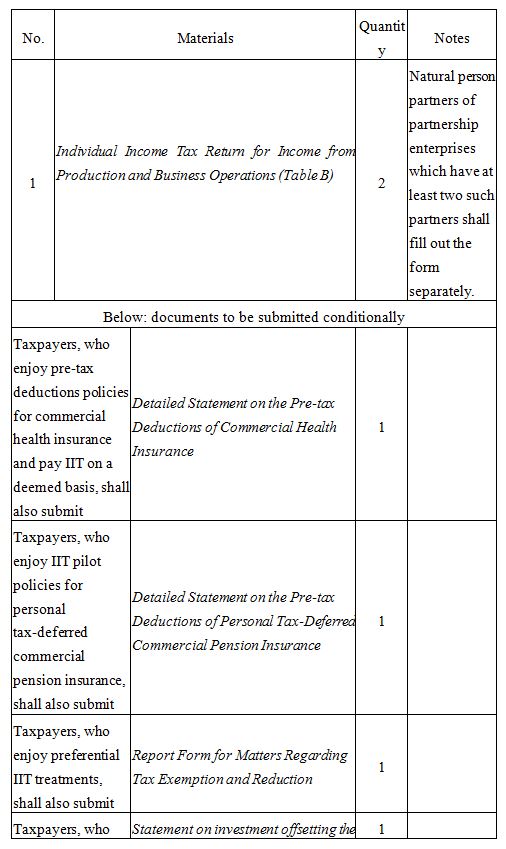

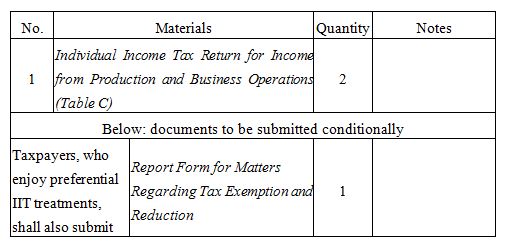

1. In caseswhere the IIT returnsof individual industrial and commercial households, operators of enterprises and public institutions as contractors or lessees, sole proprietorships, and partners of partnership enterprises, who payIIT on an actual profit basis, should be filed for prepayment, or in cases where all the aforementioned declarers who pay IIT on a deemed basis should file returns, the taxpayers shall submit:

2. In cases where IIT are paid on an actual profit basis, individual industrial and commercial households, operators of enterprises and public institutions as contractors or lessees, sole proprietorships, and partners of partnership enterprises during filing returns, shall submit:

3. In cases where income derived from two or more sources within the territory of China, from production and business operations of individual industrial and commercial households and from operationsof enterprises and public institutions as contractors or lessees,individual industrial and commercial households, operators of enterprises and public institutions as contractors or lessees, sole proprietorships, and partners of partnership enterprises, the taxpayers shall submit:

Notices for Taxpayers

1. Taxpayers are responsible for the authenticity and legitimacy of the materials submitted.

2. If the information is complete and in accordance with the legal acceptance conditions, taxpayers only need to go to the tax authority once at most.

3. Taxpayers who obtain monthly income from contracting or leasing operations shall file tax returns for the monthly (quarterly) prepayment of IIT within the first 15 days following obtainment, and file annual tax returns within 30 days after a tax year ends.

— Taxpayers who obtain income from contracting or leasing operations shall file tax returns for the monthly (quarterly) prepayment of IIT within the first 15 days following obtainment, and file annual tax returns within 3 months after a tax year ends.

— Taxpayers who pay on a deemed basis shall make a declaration within 15 days of the following month.

— Individual industrial and commercial households, sole proprietorships, and partners of partnership enterprises, who pay on an actual profit basis, shall file tax returns for the monthly (quarterly) prepayment of individual income tax within the first 15 days of the following month, and file annual tax returns within 3 months after a tax year ends.

— In cases where income is derived from two or more sources within the territory of China, from production and business operations of individual industrial and commercial households or from operations of enterprises and public institutions as contractors or lessees,the taxpayers shall combine the income under the samecategory for the computation and payment of tax and file returns on a consolidated basis within 3 months after a tax year ends.

— Taxpayers who invest in two or more enterprises (partnership enterprise included) shall file returns on a consolidated basis within 3 months after a tax year ends.

— Taxpayers, whose sole proprietorships and partnership enterprises they invest in terminate business operations in the middle of a tax year, shall make final settlement and payment within 60 days after actual termination.

4. Taxpayers with no due tax payment during any taxable period shall also file tax returns according to the relevant provisions. Taxpayers who enjoy tax exemption and reduction treatments shall file returns in accordance with relevant regulations.

5. The address of the tax service hall and websites of e-tax bureaus can be accessed through portals of provincial tax authorities and the 12366 comprehensive tax service platform.

- The State Council

- National Development and Reform Commission

- General Administration of Customs of the People's Republic of China

- National Audit Office of the People's Republic of China

- Ministry of Commerce of the People's Republic of China

- Belt and Road Initiative Tax Administration Cooperation Mechanism